The economy of India is a developing mixed economy. It is the world’s sixth-largest economy by nominal GDP and the third-largest by purchasing power parity (PPP). The country ranks 139th in per capita GDP (nominal) with $2,134 and 122nd in per capita GDP (PPP) with $7,783 as of 2018. After the 1991 economic liberalization, India achieved 6-7% average GDP growth annually. Since 2014 with the exception of 2017, India’s economy has been the world’s fastest growing major economy, surpassing China.(1)

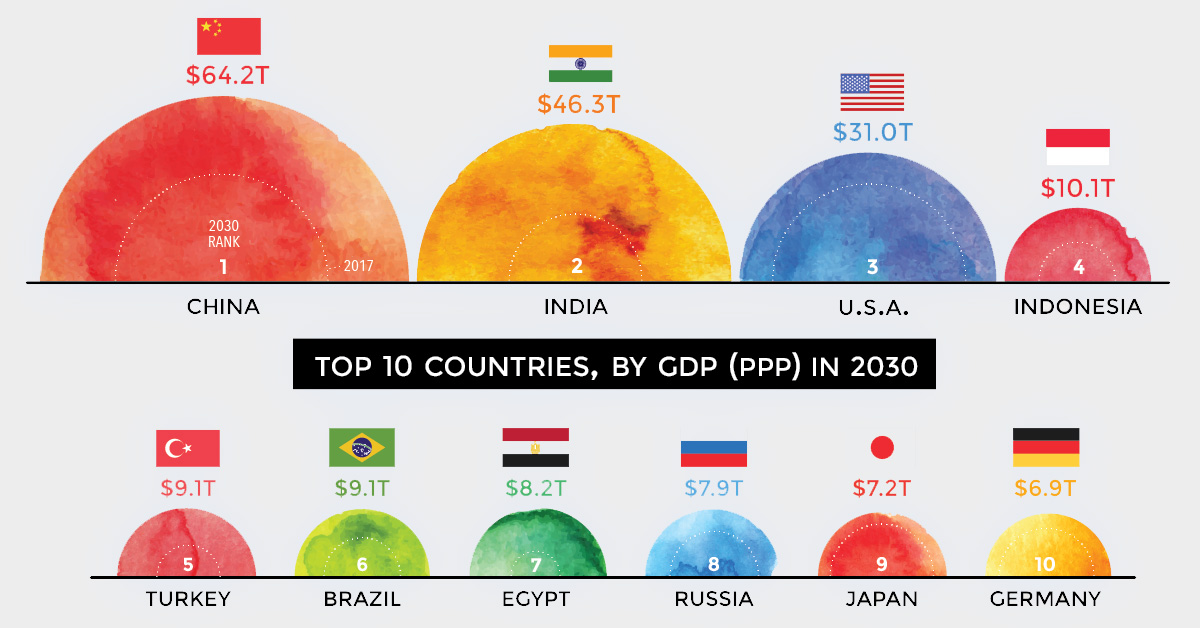

(2)The World’s Largest 10 Economies in 2030, Jeff Desjardins, January 11, 2019

https://www.visualcapitalist.com/worlds-largest-10-economies-2030/

NEW ECONOMIC POLICY

India’s economy is an ‘elephant that is starting to run’, according to the IMF

“India’s economy has enormous potential,” Shilan Shah, a senior economist at Capital Economics told the World Economic Forum in an interview. “Over the longer term the challenges are very much on the reform front, the labour market is still very dysfunctional and there hasn’t been much evidence that the government wants to tackle that.”

To spur the economy, Narendra Modi’s government has already reformed monetary policy, introduced a new banking code, as well as a goods and services tax to bolster internal trade, and taken steps to improve the business climate.

One of the most effective measures has been the introduction of one tax rate for all of India’s states, creating one internal market, Shah said, while another is the action taken to restore confidence in the banking sector. He identified structural rigidities and bureaucracy in the labour market as key barriers going forward.

“India needs to reinvigorate reform efforts to keep the growth and jobs engine running,” said Ranil Salgado, the IMF’s head of India. A “reform and streamlining of the complicated web of labour laws” could help bolster growth, he said.

The scope for improvement is further underscored by much lower per-capita income – about $2,000 per year – than that of other large emerging economies.

India – heralded by the International Monetary Fund as an “elephant starting to run” – now makes up 15% of global growth, fueled by reforms, foreign investment and strong domestic demand.(3)

HSBC’s ESTIMATES

The forecast was made by economists at HSBC Holdings Plc in a new study of 75 nations

Among HSBC’s other estimates, by 2030:

• India will pass Japan and Germany to become the third-largest economy

• Global output could be 40 percent higher than in 2017 as world growth of just below 3 percent looks sustainable

• About 70 percent of global expansion will be from emerging markets

• Austria and Norway will fall out of the top 30 due in part to their small, ageing populations

• Bangladesh will rise 16 positions to 26, while the Philippines will climb 11 slots to 27

• Africa will have more people of working age than China(4)

GLOBAL GROWTH AND INDIAN ECONOMY

The extraordinary rise of countries in Asia has spawned at least two new dynamics. First, political boundaries – many of them colonial legacies – are steadily becoming more porous through economic cooperation. Markets are converging across the Eurasian landmass as well as facilitating the geo-economic “union” of the Indian and Pacific oceans. This has resulted in new integrative dynamics; as cultures, markets and communities aspire for development and new opportunities. Second, even though territorial considerations acknowledge economic linkages, political differences are still being reasserted – not just to contest the consensus of the past, but to shape a new order altogether.

Asia is coming together economically but is also threatening to grow apart politically; market-driven growth in the region sits uneasily with a diverse array of political systems.

China is, in large part, responsible for both. While offering a political vision that stands in sharp contrast to the “liberal international order”, China has been equally assertive about advancing free trade, raising new development finance, and offering a new model for development and global governance. The prospect of China using its economic clout to advance its own norms is worrying for India.

THE EVOLUTION OF INDIA

(5)

A RISING GLOBAL POWER

IMF Country Focus interviewed Ranil Salgado, the head of the IMF team for India.

India’s economy is picking up and growth prospects look bright—partly thanks to the implementation of recent policies, such as the nationwide goods and services tax. As one of the world’s fastest-growing economies—accounting for about 15 percent of global growth—India’s economy has helped to lift millions out of poverty.

But to sustain rapid growth and raise incomes for the country’s 1.3 billion people, India will need to build on the success of its reforms, the IMF said in its annual assessment of the Indian economy.

Ranil Salgado, the head of the IMF team for India among others states:

Looking at this year’s economic assessment, you’ve likened the Indian economy to an elephant starting to run. Can you explain what you mean?

India’s economy is gaining momentum, thanks to the implementation of several recent noteworthy policies—such as the enactment of the long-awaited goods and services tax, and the country opening up more to foreign investors. Therefore, we expect economic growth to pick up to about 7.3 percent for fiscal year 2018/19—meaning the year that runs from April of 2018 through March 2019—from 6.7 percent in the year prior. Meanwhile, inflation has edged higher, in part due to a reduction of economic slack.

To sustain and build on these policies and to harness the demographic dividend associated with a growing working-age population (which constitutes about two-thirds of the total population), India needs to reinvigorate reform efforts to keep the growth and jobs engine running. This is critical in a country where per capita income is about $2,000 U.S. dollars, still well below that of other large emerging economies.(6)

THE TOP 10 FASTEST GROWING CITIES IN THE WORLD ARE IN INDIA

Think of the world’s wealthiest cities: New York, Tokyo, Los Angeles and London probably spring to mind. But based on annual gross domestic product (GDP) growth Asian cities – particularly those in India – are powering ahead of other urban economies.

According to research institute Oxford Economics, all the top 10 fastest-growing cities by GDP between 2019 and 2035 will be in India.

Surat, a large city in the northwestern state of Gujarat, will have the fastest economic growth in the world.

Surat is renowned as a diamond processing and trading centre, but it also has a strong IT sector, says the report, which predicts that the city will see an average annual GDP growth rate of 9.2% from 2019 to 2035.

In second place is Agra – home of the Taj Mahal – which will grow by 8.6% year on year.

Bengaluru – known as India’s Silicon Valley because of its booming tech and start-up scene – will grow 8.5% year on year by 2035, putting it in third place.

Hyderabad, another Indian tech hub, is in fourth place with 8.47% growth. The southern city is also home to the country’s first IKEA store.

India’s dominance of the list of fastest-growing cities illustrates the broader theme of the tipping of economic might from West to East, the authors argue.(7)

UN: INDIA WILL HAVE 7 MEGACITIES BY 2030

India is a key topic at the World Economic Forum’s Annual Meeting 2017. Watch the session on India’s Turn to Transform here.

The noise and bustle on the streets of India’s biggest cities is a defining characteristic of a country that’s home to over a billion people.

Every year, millions more leave their traditional homes in rural towns and villages and head into urban areas. The United Nations World Cities Report 2016 says 9.6 million people will move to New Delhi by 2030.

To qualify as a megacity under the UN definition, an urban area must have a population of 10 million people. The UN takes into account urban sprawl and measures populations beyond official city limits. On these criteria, India currently has five megacities.

1. New Delhi The capital city has a population of 26.5 million people

2. Mumbai India’s financial hub has a population of 21.4 million people

3. Kolkata An important trading hub, with 15 million people living in urban area

4. Bengaluru The ‘Silicon Valley’ of India; 10.5 million people call it home

5. Chennai Home of the Indian motor industry, as well as 10.2 million people

Other urban areas in India are growing rapidly as people look to cities for jobs and financial security, as well as the chance of a better education for their children. This rural-to-urban migration will result in two more urban areas becoming megacities by 2030, says the UN.

1. Hyderabad A strong IT hub and tourism centre. It may be home to 12.8 million by 2030

2. Ahmedabad The heart of the textile industry is expected to house 10.5 million by 2030

Megacities and mega-slums

Many millions of people who move to India’s growing cities will miss out on the economic benefits of urban living. The UN report says the number of people living in slums across the developing world rose from 689 million to 880 million between 1990 and 2014. The Dharavi slum in Mumbai is home to an estimated one million people. New arrivals are not totally deprived of opportunities, however. According to the Economic Times of India, the slum has an economic output estimated at $1 billion a year.

Image: UN World Cities Report

The drift from rural to urban living is not exclusive to India; it’s happening across the developing world. The UN report says 500 million people currently live in 31 megacities around the world.

What’s more, the number of cities with populations of more than 10 million people will rise to 41 by 2030. Most of that growth will happen in Asia and Africa. The two continents will be home to 33 of those 41 megacities by 2030.(8)

INDIA IS BUILDING A BRAND NEW CITY

Gujarat International Finance-Tec City – or ‘GIFT’ for short – is a present for the Indian financial services sector.

The brand new city is designed to help India compete with international and regional finance hubs, such as Hong Kong and Singapore. The team behind the project hope it will appeal to global firms by providing high-class infrastructure and facilities, with a stream of top Indian talent to fill jobs.

The opportunity is significant: India’s financial sector is growing rapidly, and could generate 11 million jobs and contribute up to $400 billion to GDP by 2020, according to the group behind the project.

An artist’s plan of how the city will look when complete.

Fintech is a new Central Business District (CBD)

The plan is to build a Central Business District (CBD) between Ahmedabad and Gandhinagar in the west of the country, with state-of-the-art connectivity, infrastructure and transport links.

Some tower blocks have already been built.

By attracting international investment, the city’s developers estimate they could provide a million direct and indirect jobs, in areas including capital markets, trading and IT services.

The city also hopes to take advantage of rapid economic growth, with the IMF forecasting growth of more than 7% for the current fiscal year which ends in March 2019.And the appeal of a financial services hub is clear. Take the City of London, for example, which was responsible for 50% of the UK sector’s output in 2017 and provided 1.1 million jobs.(9)

THE SOURCES FOR THE COMPLETE ARTICLES:

(1) en.wikipedia.org/Economy_of_India

(2) www.visualcapitalist.com/worlds-largest-10-economies-2030

(3) www.weforum.org/2018/how-india-could-supercharge-its-economy

(4) www.bloomberg.com/china-economy-set-to-pass-u-s-as-number-one-by-2030

(5) www.weforum.org/what-is-indias-vision-for-the-world-modi

(6) www.imf.org/India-Strong-Economy-Continues-to-Lead-Global-Growth

(7) www.weforum.org/top-10-cities-with-the-fastest-growing-economies-will-be-in-india

(8) www.weforum.org/india-megacities-by-2030-united-nations

(9) www.weforum.org/india-is-building-a-city-from-scratch-to-attract-foreign-investors

All the articles from the WORLD ECONOMIC FORUM, BLOOMBERG and I.M.F. are originally published in their complete editions as described above.

More articles about India can be found in the W.E.F. in the sections: The Agenda / India and the India Economic Summit 2017.

www.weforum.org/agenda/archive/india

www.weforum.org/events/india-economic-summit-2017#

Kallirroi Pavlakou

International News and Markets